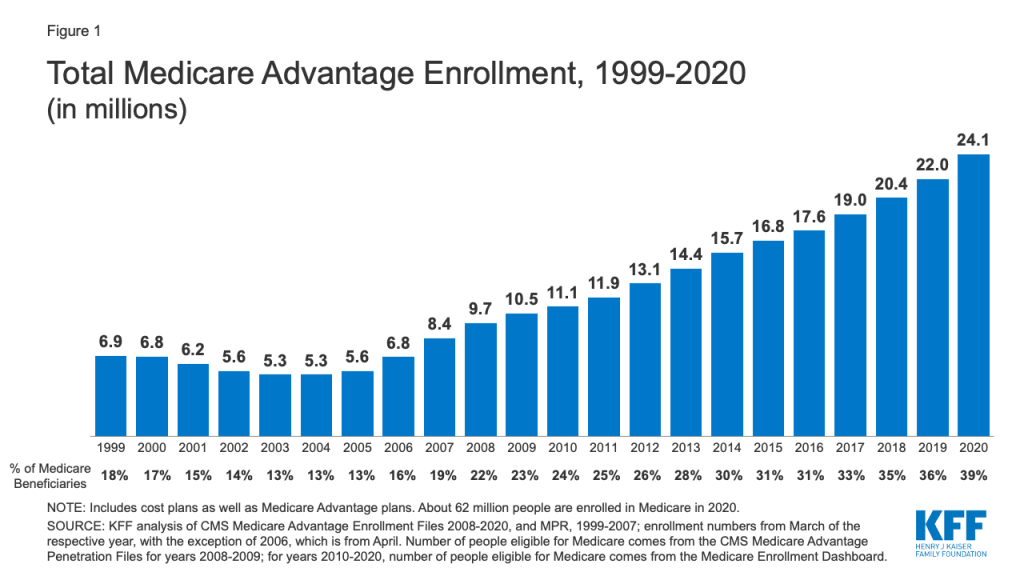

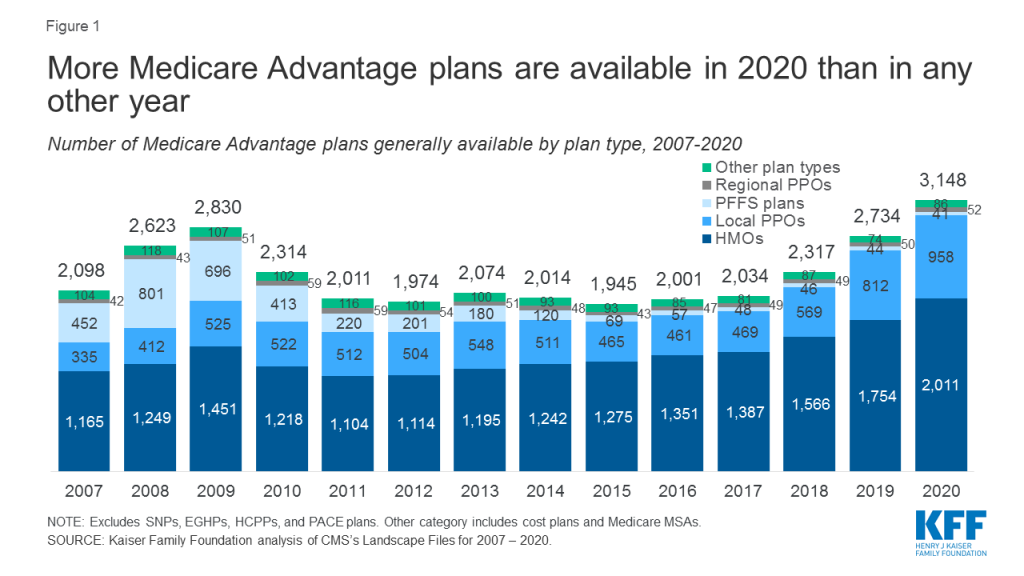

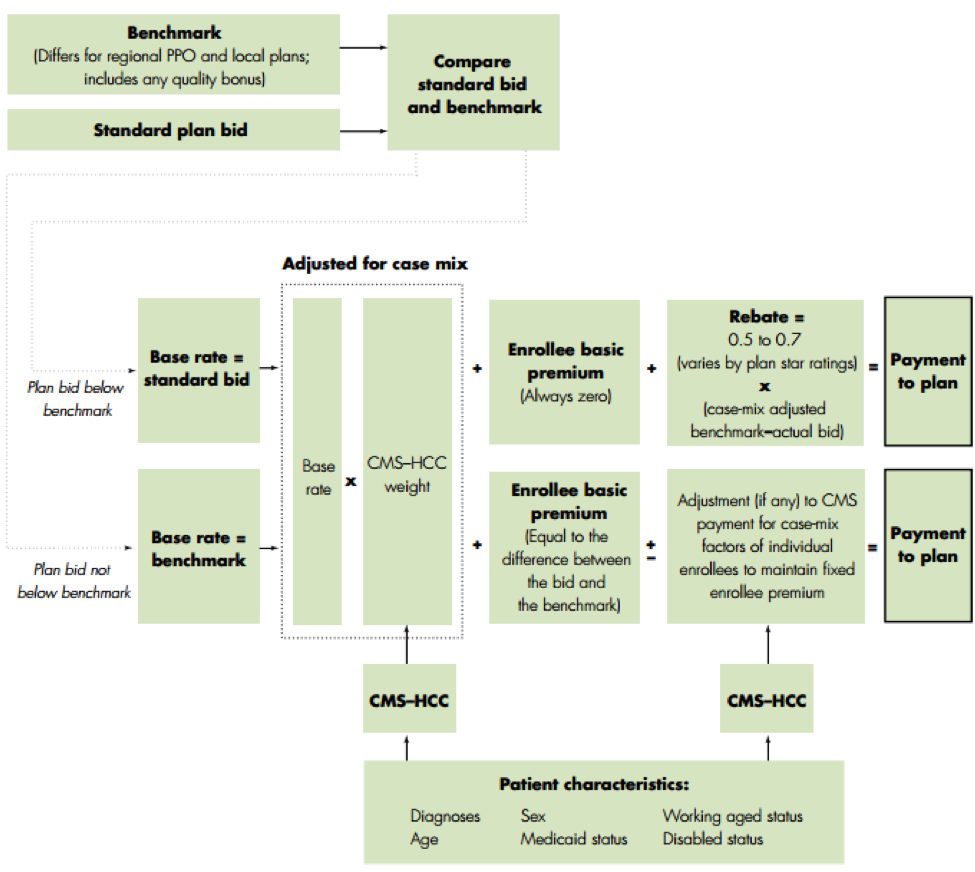

class: center, middle, inverse, title-slide # How Does Insurance Competition Affect Medical Consumption ## Presenter: Conor Ryan ### Discussant: Ian McCarthy ### ASHEcon Annual Meeting, June 21, 2021 --- <!-- Adjust some CSS code for font size, maintain R code font size --> <style type="text/css"> .remark-slide-content { font-size: 30px; padding: 1em 2em 1em 2em; } .remark-code, .remark-inline-code { font-size: 20px; } </style> <!-- Set R options for how code chunks are displayed and load packages --> # Medicare .center[  ] --- count: false # Medicare - Introduced in 1965 - Private Medicare plans authorized in 1972 (started in 1976) - Medicare + Choice formalized in 1997 - Medicare Advantage and Part D in 2003 (started in 2006) --- # Medicare Advantage Growth .center[  ] --- # Medicare Advantage Plan Types .center[  ] --- # Medicare Advantage Key Points 1. Huge growth 2. Almost entirely managed care plans now 3. Almost all plans offer prescription drug coverage (90% in 2020) 4. Almost all plans have $0 premium for Part C coverage --- # Bidding Process .center[  ] --- # Final thoughts and questions - Part C and Part D bidding processes are separate. - Does the insurer "choose" a premium? Or do they choose a bid? - Are co-pays set directly or determined after bid submission? - Where does prescription drug coverage fit here? - What about the quality rating system? Generates bonuses and extra percentage for rebates. - Do firms "exploit" inertia in premium and co-payment setting?