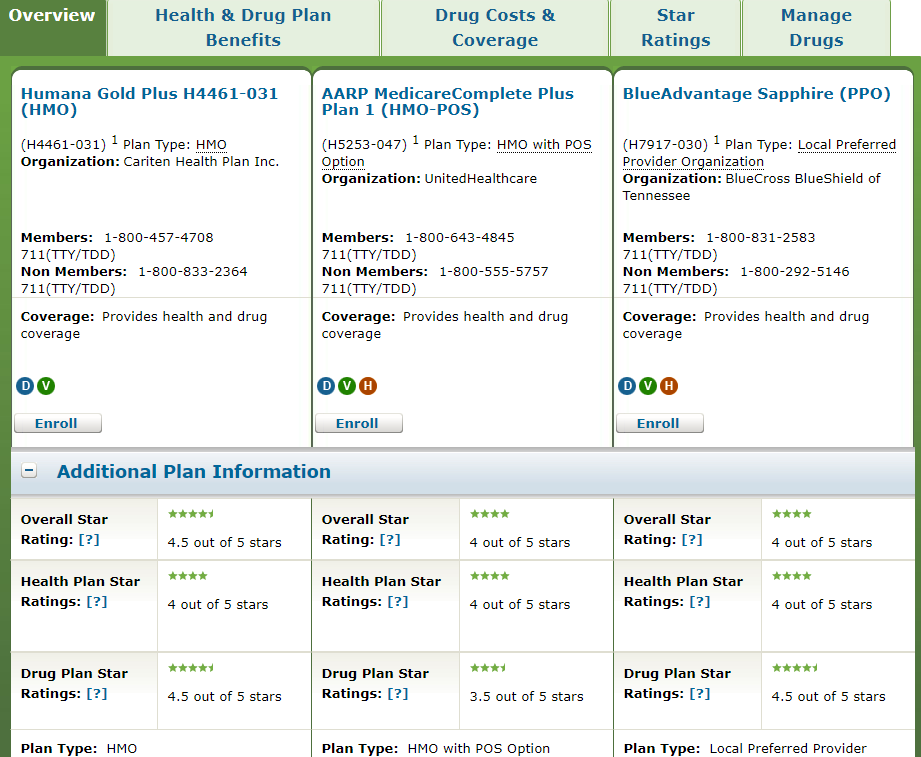

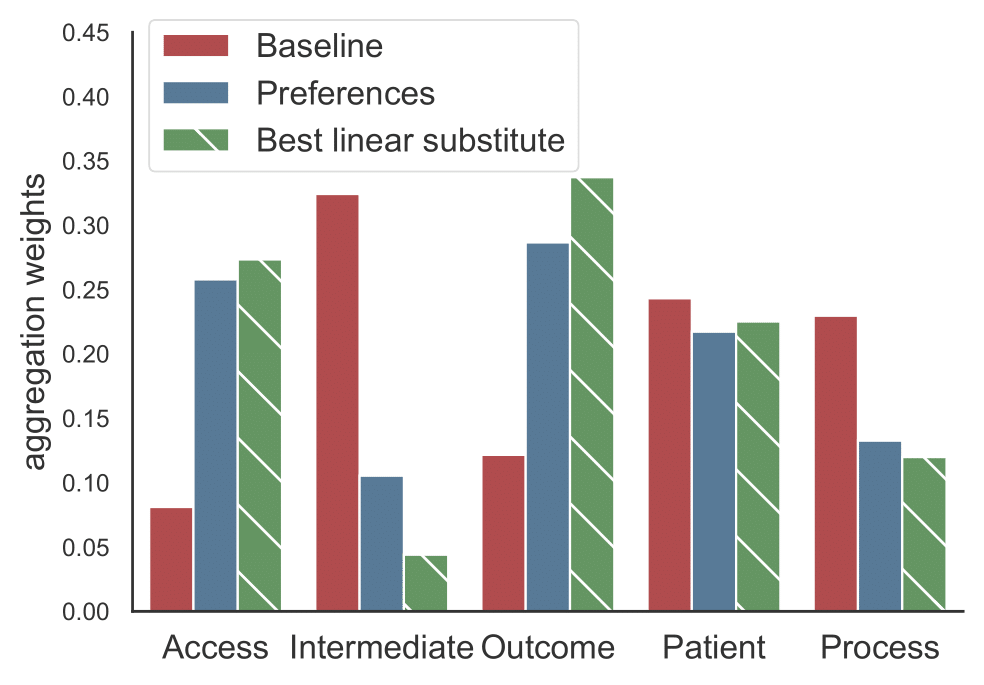

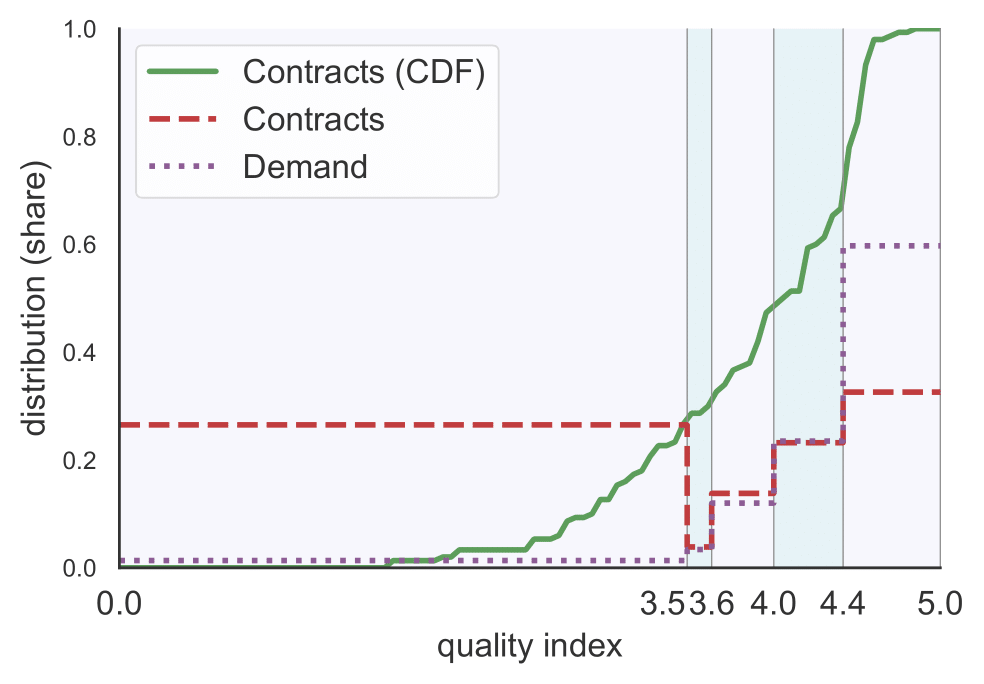

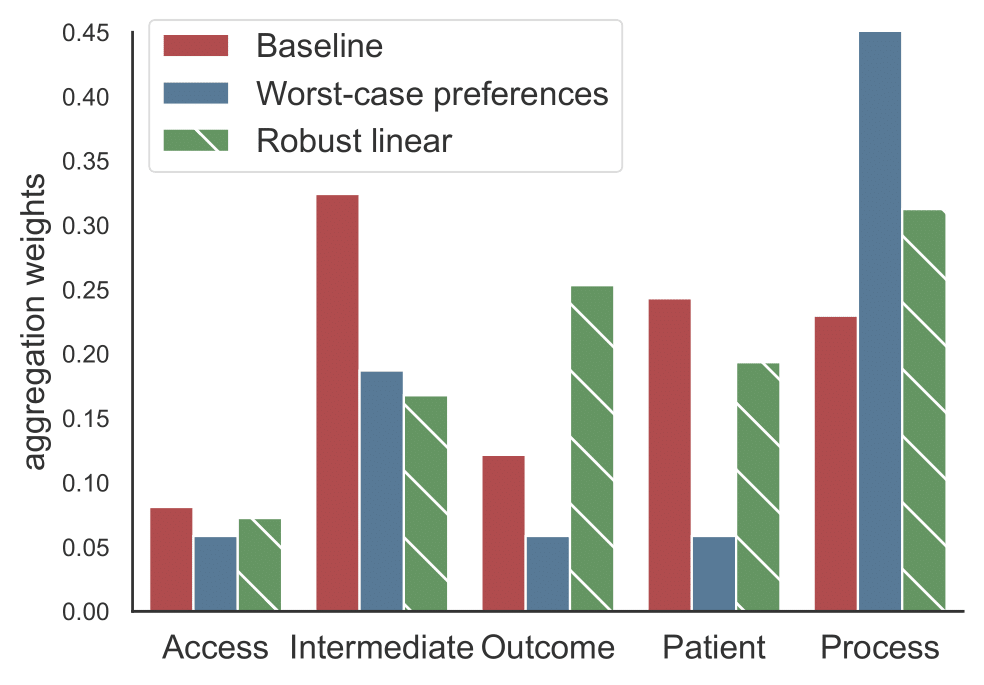

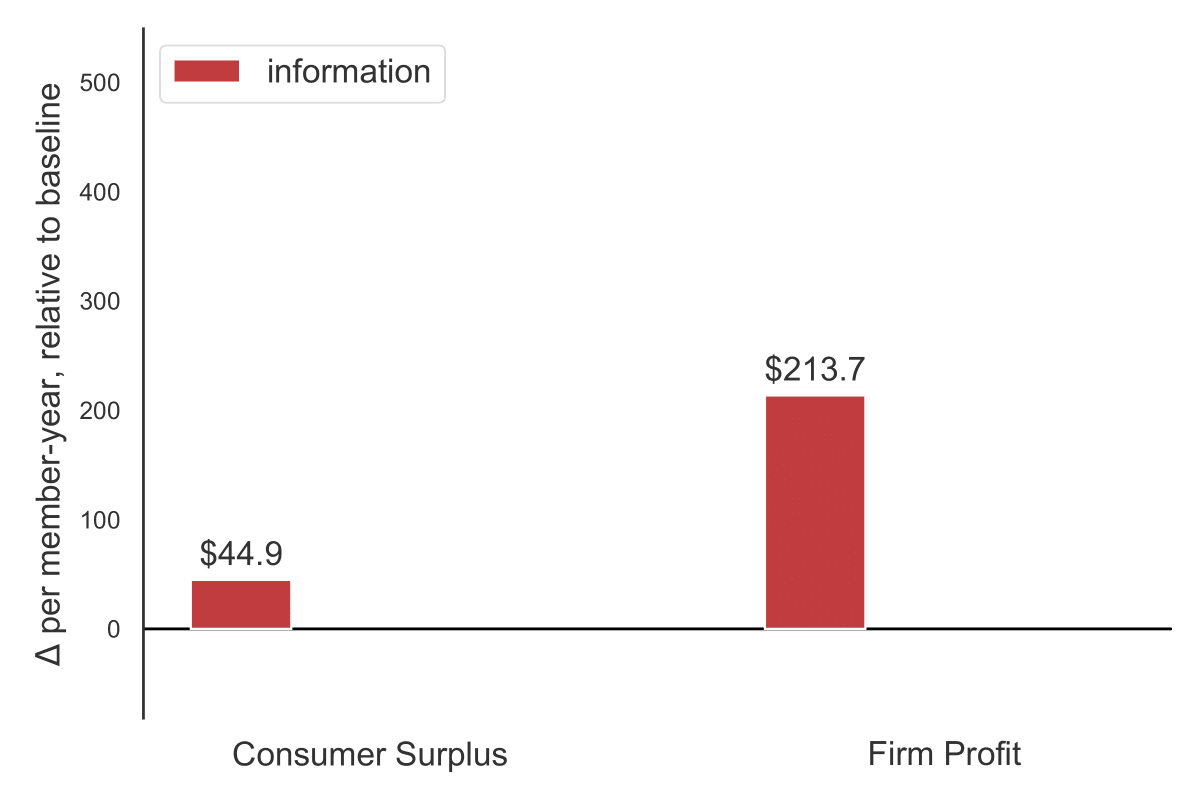

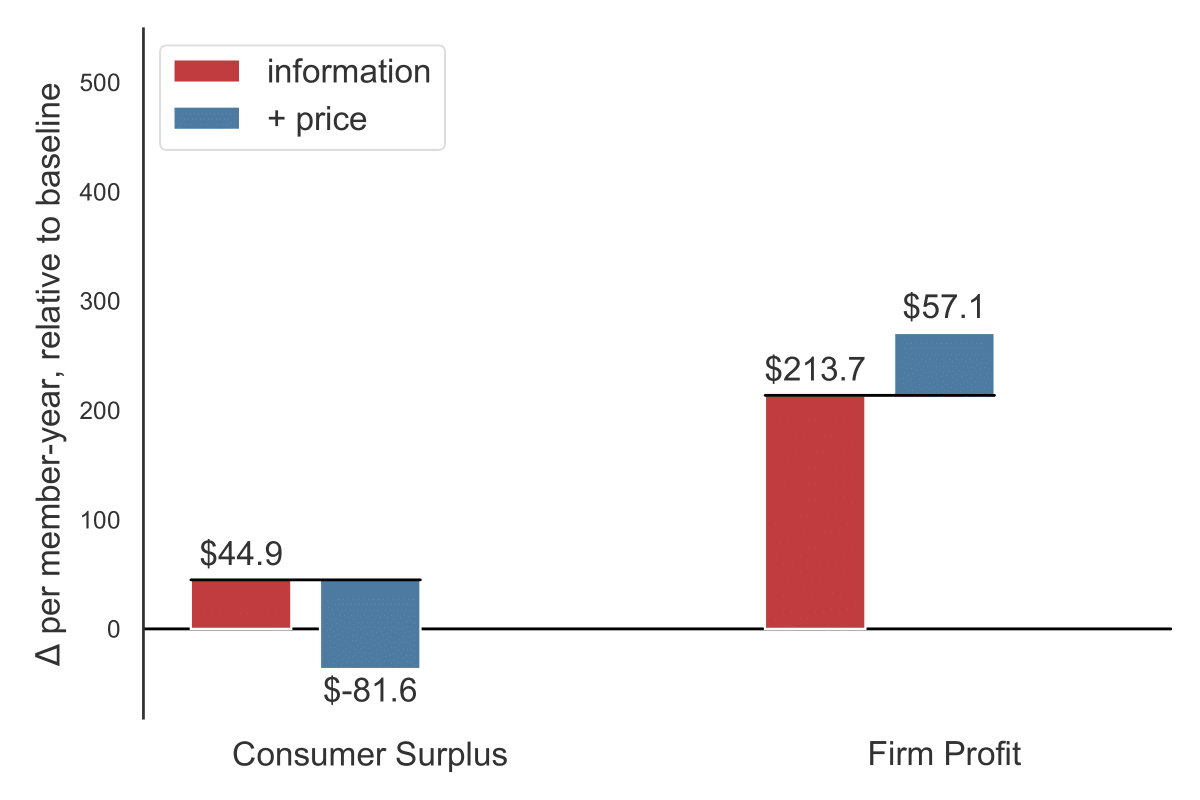

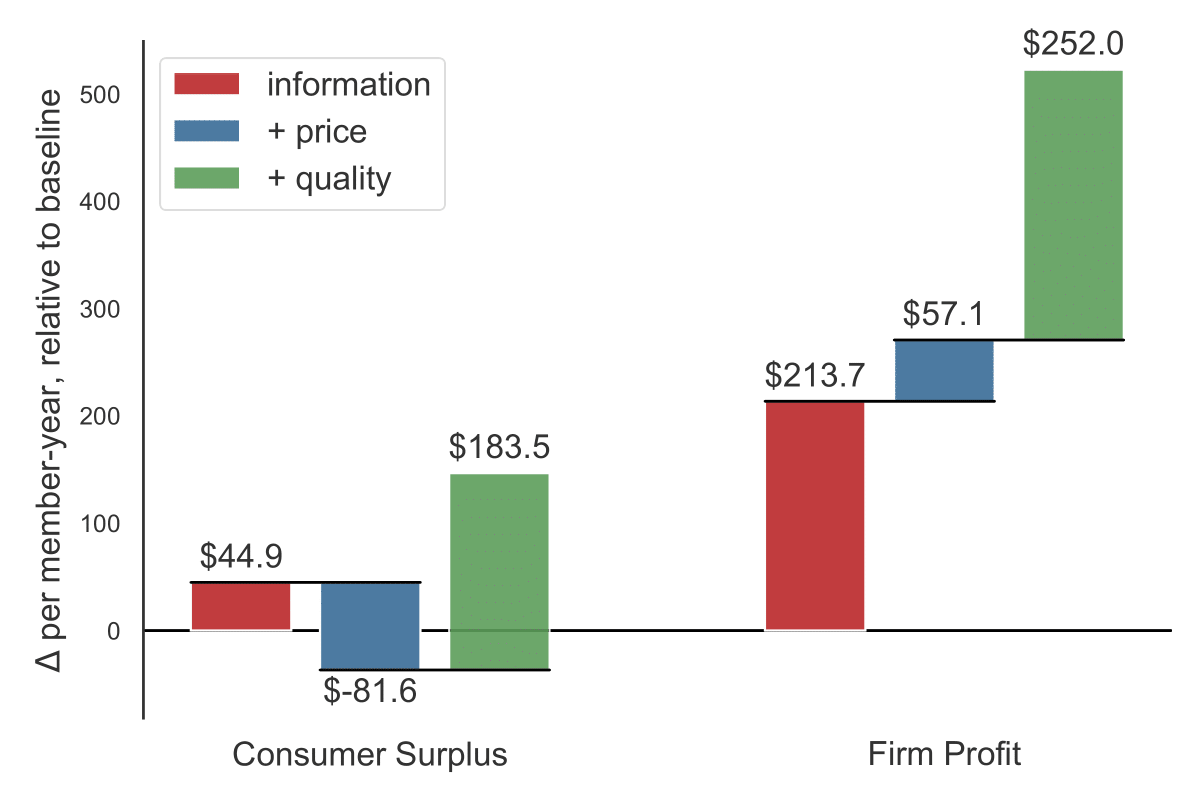

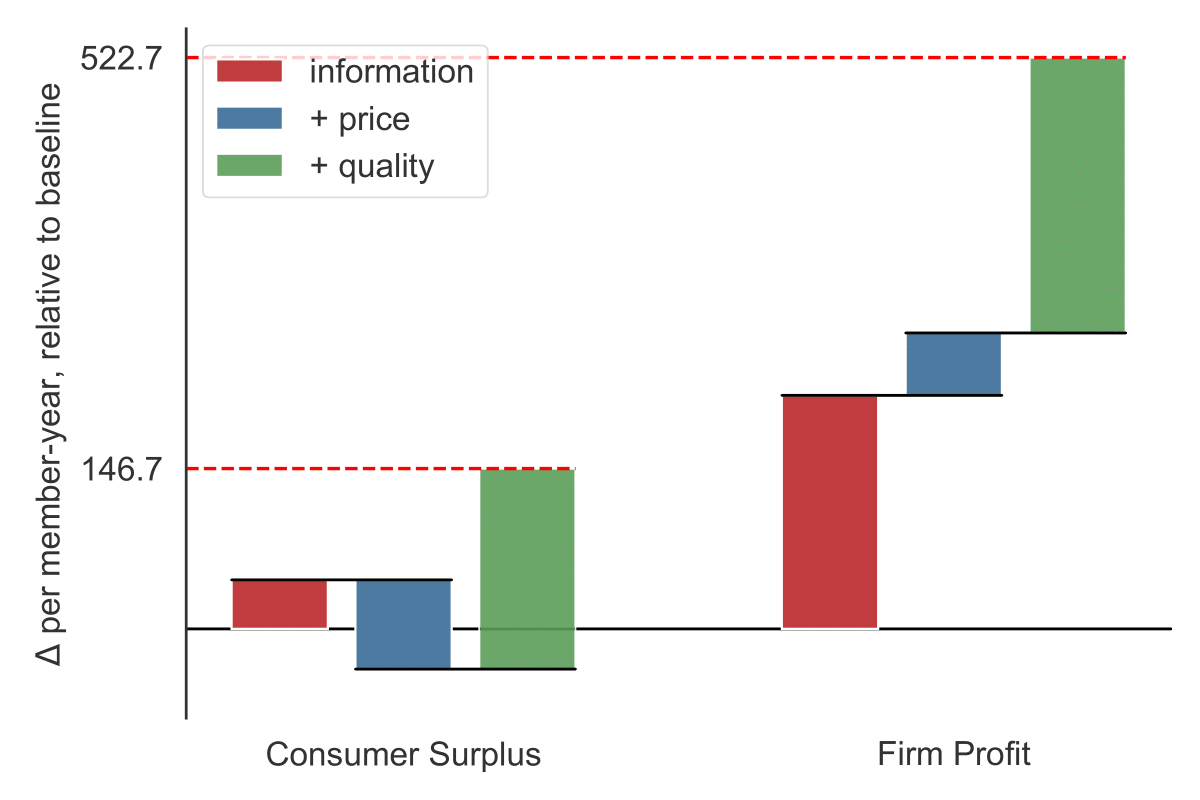

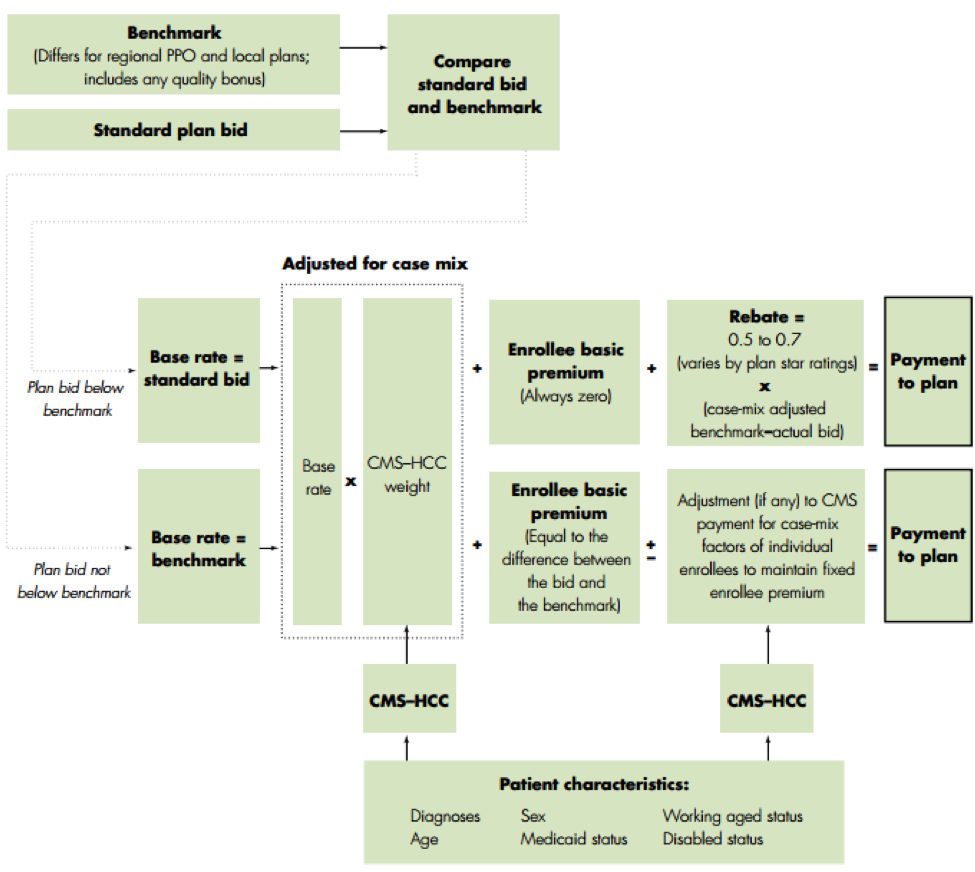

class: center, middle, inverse, title-slide .title[ # Quality Disclosure and Regulation ] .subtitle[ ## Scoring Design in Medicare Advantage ] .author[ ### <strong>Author:</strong> Benjamin Vatter, Stanford University (MIT upcoming) ] .author[ ### <strong>Discussant:</strong> Ian McCarthy, Emory University and NBER ] .date[ ### AHEW, October 1, 2022 ] --- class: inverse, center, middle <!-- Adjust some CSS code for font size, maintain R code font size --> <style type="text/css"> .remark-slide-content { font-size: 30px; padding: 1em 2em 1em 2em; } .remark-code, .remark-inline-code { font-size: 20px; } </style> <!-- Set R options for how code chunks are displayed and load packages --> # What's the point? <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- # 1. Endogenous quality (Spence, 1975) - **Setting:** Monopoly (or oligopoly) when firms set both price and quality - **Intuition:** Firm invests to the point where marginal quality valuation meets marginal costs of quality, but socially optimal quality depends on average valuation - **Takeaway:** Profit-maximizing quality will differ from socially optimal quality when the marginal customer is not representative of the average -- Natural in the presence of adverse selection, where the marginal patient is almost always different from the average patient --- # 2. Types of quality disclosure - Self-disclosed quality via advertising - Word-of-mouth and aggregated reviews form users (Google, Rotten Tomatoes, etc.) - Third-party rating agencies - **Government regulation via mandated disclosure or licensing** --- # The main idea - Need some form of quality disclosure to aid decision making - Full-disclosure likely yields under-investment in quality -- - Regulator can improve quality via coarse rating scores - but...firms will respond to the scoring design accordingly --- class: inverse, center, middle # Context <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- # Medicare Advantage .pull-left[  ] .pull-right[  ] --- # Selecting an MA plan When someone nears 65, they'll receive: - Medicare & You Booklet (128 pages in 2022) - Points beneficiary to Medicare's online plan finder tool - **Lots** of other marketing materials touting different types of plans - Standalone Part D plans - Medicare supplemental plans - Medicare Advantage plans - Assume someone has decided to search for an MA plan online --- class: clear .center[  ] --- class: clear .center[  ] --- class: clear .center[  ] --- class: clear .center[  ] --- class: clear .center[  ] --- class: clear .center[  ] --- class: clear .center[  ] --- class: clear .center[  ] --- class: inverse, center, middle # Preview of findings <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- class: clear 1. Estimate structural model of price **and quality investments** 2. Identify optimal scoring design -- .pull-left[  ] .pull-right[  ] --- # Some points of applause - Substantial contribution, both theoretical and empirical - Highly policy relevant -- "To address this, I completed the data by reviewing a decade of public communications by CMS aimed at insurers. I recover year-to-year changes to the scoring design, **replicating the public scoring assignment perfectly.**" --- class: inverse, center, middle # Setup and estimation <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- class: clear <img src="ahew-2022-vatter_files/figure-html/tikz-timeline-1.png" style="display: block; margin: auto;" /> --- class: clear <img src="ahew-2022-vatter_files/figure-html/tikz-new-1.png" style="display: block; margin: auto;" /> **What's new here?** - Endogenous quality investments with imperfect mapping into quality scores - Endogenous scoring design --- class: clear <img src="ahew-2022-vatter_files/figure-html/tikz-4-1.png" style="display: block; margin: auto;" /> `$$u_{ij} = \underbrace{\alpha_i P_{j}}_{\text{premium}} + \underbrace{\beta_i b_{j}}_{\text{coverage}} + \underbrace{\mathcal{E}_{\psi}[\boldsymbol{\gamma}'\boldsymbol{q}|\psi(q_{j})]}_{\text{quality}} + \underbrace{\lambda'z_{ij}}_{\substack{\text{Obs.}\\\text{attributes}}} + \underbrace{\xi_{j}}_{\substack{\text{unobs.}\\\text{preferences}}} + \underbrace{\varepsilon_{ij}}_{\sim \text{T1EV}}$$` Note: when you see `\(j\)`, think `\(jmt\)` --- # Demand estimation `$$u_{ij} = \underbrace{\alpha_i P_{j}}_{\text{premium}} + \underbrace{\beta_i b_{j}}_{\text{coverage}} + \underbrace{\mathcal{E}_{\psi}[\boldsymbol{\gamma}'\boldsymbol{q}|\psi(q_{j})]}_{\text{quality}} + \underbrace{\lambda'z_{ij}}_{\substack{\text{Obs.}\\\text{attributes}}} + \underbrace{\xi_{j}}_{\substack{\text{unobs.}\\\text{preferences}}} + \underbrace{\varepsilon_{ij}}_{\sim \text{T1EV}}$$` -- Two(three)-step process: 1. Estimate mean preferences, `\(\hat{\delta}_{j}\)`, from `\(u_{ij} = \color{red}{\delta_{j}} + \color{blue}{\kappa_{ij}} + \varepsilon_{ij}\)` 2. TSLS regression of `\(\hat{\delta}_{j}\)` on observable characteristics and fixed effects. 3. (if needed) Estimate preference for quality by minimizing the square difference between a contract fixed effect and expected quality, `\(\eta_{j} - \boldsymbol{\gamma} \mathcal{E}[\boldsymbol{q} | r, \psi]\)`, across time periods (pairwise time period differences). --- # Question/concern Estimating preferences for quality... - within an estimated fixed effect, `\(\hat{\eta}\)` - within an estimated mean preference, `\(\hat{\delta}\)` -- - What does the distribution of these fixed effects look like? - How much variation exists in **within-contract** quality (or expected quality) over time? --- class: clear <img src="ahew-2022-vatter_files/figure-html/tikz-3-1.png" style="display: block; margin: auto;" /> `$$\pi_{f}(\boldsymbol{q}, \psi) = \max_{\{p_j\}_{j \in J_{f}}} \sum_{j \in J_{f}}\underbrace{D_{j}(\boldsymbol{p}, \psi(\boldsymbol{q}))}_{\text{demand}} (\underbrace{R_j(p_j)}_{\text{mg. revenue}} - \underbrace{C(\boldsymbol{q}_j, \boldsymbol{z}_{j}, \boldsymbol{\theta}_j)}_{\text{mg. cost}})$$` --- # Pricing (insurance costs) estimation `$$\pi_{f}(\boldsymbol{q}, \psi) = \max_{\{p_j\}_{j \in J_{f}}} \sum_{j \in J_{f}}\underbrace{D_{j}(\boldsymbol{p}, \psi(\boldsymbol{q}))}_{\text{demand}} (\underbrace{R_j(p_j)}_{\text{mg. revenue}} - \underbrace{C(\boldsymbol{q}_j, \boldsymbol{z}_{j}, \boldsymbol{\theta}_j)}_{\text{mg. cost}})$$` -- - Profit maximization yields standard `\(MR=MC\)` expression - Recover marginal costs - Decompose marginal costs into part due to quality, other observable components, and residual, `$$MC=\boldsymbol{\theta}^{c}_{q}\boldsymbol{q} + \boldsymbol{\theta}_{a}^{c}\boldsymbol{a} + c$$` --- class: clear <img src="ahew-2022-vatter_files/figure-html/tikz-2-1.png" style="display: block; margin: auto;" /> `$$\max_{\boldsymbol{x}_f \in \mathbb{R}^{|\mathcal{Q}| \times |J_f|}} \underbrace{\int E\left[\pi_{f}(\boldsymbol{q}_f, \boldsymbol{q}_{-f}, \psi)\right] dF(\boldsymbol{q}_f|\boldsymbol{x}_f)}_{\text{expected insurance profit}} - \underbrace{I(\boldsymbol{x}_f, \boldsymbol{\mu}_{\boldsymbol{f}})}_{\text{investment cost}}$$` --- # Quality (investment costs) estimation `$$\max_{\boldsymbol{x}_f \in \mathbb{R}^{|\mathcal{Q}| \times |J_f|}} \underbrace{\int E\left[\pi_{f}(\boldsymbol{q}_f, \boldsymbol{q}_{-f}, \psi)\right] dF(\boldsymbol{q}_f|\boldsymbol{x}_f)}_{\text{expected insurance profit}} - \underbrace{I(\boldsymbol{x}_f, \boldsymbol{\mu}_{\boldsymbol{f}})}_{\text{investment cost}}$$` - Equate marginal revenue from quality investment with marginal investment cost - Assume investment costs are quadratic and **separable across products and categories** --- # Question/concern - Costs almost surely are **not** separable across categories - Investment in network changes access, outcomes, patient surveys - Investment for one contract likely spills over into other contracts for same insurer - How much does this matter? --- class: clear <img src="ahew-2022-vatter_files/figure-html/tikz-1-1.png" style="display: block; margin: auto;" /> `$$\max_{\psi \in \Psi} E_{\boldsymbol{q}}[\underbrace{CS(\psi, \boldsymbol{q})}_{\substack{\text{Consumer}\\\text{surplus}}} + \rho^{F}\underbrace{\sum_{f}V_f(\psi, \boldsymbol{q}) - I(\boldsymbol{x}_f^*(\psi), \mu_f)}_{\substack{\text{Insurer}\\\text{profit}}} - \rho^{G}\underbrace{Gov(\psi, \boldsymbol{q})}_{\substack{\text{Government}\\\text{spending}}} \vert \boldsymbol{x}^*(\psi)]$$` --- # Scoring design estimation `$$\max_{\psi \in \Psi} E_{\boldsymbol{q}}[\underbrace{CS(\psi, \boldsymbol{q})}_{\substack{\text{Consumer}\\\text{surplus}}} + \rho^{F}\underbrace{\sum_{f}V_f(\psi, \boldsymbol{q}) - I(\boldsymbol{x}_f^*(\psi), \mu_f)}_{\substack{\text{Insurer}\\\text{profit}}} - \rho^{G}\underbrace{Gov(\psi, \boldsymbol{q})}_{\substack{\text{Government}\\\text{spending}}} \vert \boldsymbol{x}^*(\psi)]$$` - Designer chooses scoring rule, `\(\psi\)`, from class of rules, `\(\boldsymbol{\Psi}\)` - Trades off information for efficiency - Paper shows that any monotone partitional score reduces to two elements: an aggregator and a cutoff function - Considers optimal design among the set of designs with no more than 15 partitions and quadratic aggregators, setting `\(\rho^{F}=1\)` and `\(\rho^{G}=0\)`, for year 2015 --- # Question/concern - Do optimal cutoffs and aggregator change in different years? - With different `\(\rho^{F}\)` and `\(\rho^{G}\)`? - No firm response to quality bonuses, but costs to CMS could be in `\(\rho^{G}\)` --- class: inverse, center, middle # Main results <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- # Demand .center[  ] --- # Supply | Category | Insurance Costs, `\(\theta_{q}\)` | Investment Costs, `\(\mu_{k}\)` | | ------------- | ---------------------------------:| ---------------------------:| | Access | 31.16 | 15.620*** | | Intermediate | 108.40*** | 19.530*** | | Outcome | 16.810*** | 15.000*** | | Patient | -244.30*** | 14.730*** | | Process | -175.60*** | 1.106 | --- # Scoring design .pull-left[  ] .pull-right[  ] - Optimal design involves linear aggregator among 5 partitions - Pooling at the bottom, with very little demand for low-quality plans - Closely matches consumer WTP (except for Intermediate category?) - **Question:** How much is 3.5 vs 3.6 just noise? --- # Scoring design with uninformed beneficiaries .pull-left[  ] .pull-right[  ] - Is CMS pretty close already? - Current design seems consistent with some feasible set of preferences - Would be very interesting to know under what preferences the current design is actually optimal --- # Welfare .center[  ] --- # Welfare .center[  ] --- # Welfare .center[  ] --- # Welfare .center[  ] --- # Welfare .center[  ] --- class: inverse, center, middle # Considerations for this paper (not necessarily actionable) <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- # The bid process .pull-left[  ] .pull-right[ - Not just setting price - Separate Part D bid process - Ability to use Part C rebate to go toward Part D premium ] --- # Contracts vs plans - Beneficiaries choose plans, defined by specific premium and benefits - Quality is measured by contract -- - Paper argues that there is really only one plan per contract - Makes sense in recent years but maybe not in early years - Can't have it both ways - Price variation within contract good - but product differentiation within given quality score irrelevant? --- # Scoring design Does (should) the setup incorporate... - Bonuses for high scores? **No** - Contract consolidation of plans? **No** - Part D quality? **No** - Penalty for high-variance contracts (i-factor)? **Maybe** - Alert for ratings below 3 stars or at 5 stars? **Maybe** --- # Scoring design More fundamental questions... - Are ratings reflective of quality? How do we define a "good" health insurance plan? - Is the rating monotonically increasing in underlying quality? -- .center[  ] --- class: inverse, center, middle # Considerations for more papers <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- # 1. Measuring quality - What's the best way to measure the underlying quality score? - Many of the current measures are provider (network) specific - Relates to the *aggregator* in current framework, but would not take current categories (or construction of current categories) as given --- # 2. Policy uncertainty - Can some policy uncertainty avoid bunching just above the threshold values? - How much policy uncertainty is optimal? - How do insurers respond to such uncertainty? -- - Already in the model: mapping between quality investments and the quality score - Already in the data: introduction of new measures and publication of specific threshold values for some measures --- # 3. Learning about scoring designs - The scoring designs are complicated - Likely takes time for insurers to understand the policy and update plans/contracts accordingly --- class: inverse, center, middle # Final thoughts <html><div style='float:left'></div><hr color='#EB811B' size=1px width=1055px></html> --- class: clear, center